Risk is an abstract thing. It’s defined as the possibility of something bad happening. Risk involves uncertainty about the effects and implications of an activity, especially when it concerns something we value (such as health, well-being, wealth, property, or the environment). It often focuses on negative, undesirable consequences. The problem with risk is that it is fluid and, for many investors, it is a concept that we are told, but cannot fully grasp even when it is illustrated with charts and numbers until we are neck-deep in it.

As children, we learn to deal with risk and manage it. Take crossing the street, for example. At first, this is an anxious affair. Our parents warn us to look both ways, and we learn to proceed cautiously. Over time, we learn to cross with ease and are no longer anxious.

Caution is rationale and sensible. There are still risks buried somewhere deep in the act of crossing the street. We learn to deal with that risk by looking both ways even when the traffic light is green and on our side. The truth is, we haven’t eliminated the risk of crossing the road, we’ve simply learned to manage it and keep it within a comfortable tolerance.

We all appreciate the concept of risk when it comes to crossing the street. Afterall, we will have crossed streets thousands of times by the time we are adults. Some of us, though, may choose to ignore or defy the risks by darting recklessly between cars to gain a few more seconds. When it comes to money, however, I fear that the concept is still fleeting. As individual investors, we just don’t have the experience of having been through thousands of bear market cycles to understand how to assess and manage our risks. As a result, we have the unfortunate consequence of having cognitive and emotional behavioural biases that affect our thinking and, therefore, impact our decision making. Said another way, most investors don’t understand the difference (or risks) between darting between cars to possibly gain a few extra seconds, compared to waiting for the light to turn green and still look both ways before crossing.

Rock-Climbing, Investing and Risk

So how does this apply to managing your money?

Your March 31, 2020 statement will likely show that your account is worth $x-amount less than it was on December 31, 2019. “I’ve lost $x! That doesn’t sound like risk management to me!”, you might say. I understand. So, let me illustrate. I received my 2020 special edition of Rock and Ice magazine last Friday, and its glossy pages of outdoor heaven inspired me to give you a rock-climbing analogy. (If you watched the movies I mentioned in my last commentary - The Dawn Wall and Free Solo - about Tommy Caldwell & Kevin Jorgeson (The Dawn Wall) and Alex Honnold (Free Solo) - you will appreciate the following example even more.

Picture yourself several hundred feet above the ground on the side of a mountain face, battling gravity with only millimetres of skin and rubber. You are protected by a single rope, a few carabiners and some bolts embedded into the cliff wall. How would you feel? Uncomfortable, I would imagine. And, for many of us, absolutely terrified at even the thought. Risk comes to mind, doesn’t it? Risk is easy to imagine in this instance. What happens if my hand or foot slips? What if I get tired? Will the bolt hold? Is my partner paying attention and prepared? Now imagine being on the same cliff face, without a partner or any protection. The risks are greater now, are they not? It’s easy to imagine how different a fall in each instance would be. This is risk, and it is embedded in our lives every day. Whether we are professional, elite rock-climbing athletes, like Tommy, Kevin, or Alex, or the average person crossing a street, there is risk in everything we do. Risk can be managed and kept within a range of defined outcomes, but it can never be completely controlled.

|

Alex Honnold, Free soloing the Free Rider route (5.12d) on El Capitan, Yosemite National Park |

|

Tommy Caldwell and Kevin Jorgeson Free climbing the Dawn Wall on El Capitan, Yosemite National Park |

I admire Alex Honnold for his amazing accomplishments and skill as an athlete and for teaching me what we can accomplish as humans. I completely understand that you might see free solo rock climbing as reckless behaviour, akin to darting between cars. However, Alex is extremely meticulous in his preparation, having spent years free climbing that same wall, perfecting, rehearsing, and memorizing exact sequences of hand and foot placements for every key pitch. He is a habitual note-taker, logging his workouts and evaluating his performance on every climb in a detailed journal.In the case of investment management, no matter our experience, track record or encouragement from our throngs of adoring fans (okay, I made up the last part), we never want to free solo with our client’s assets. No matter how certain and convinced we are, the markets have a way of humbling us, and the consequences of not controlling for risk are too great.

However, in the investment world, no matter how prepared we are, we cannot control every variable with perfection. We do not have the benefit of practicing the same route (i.e. managing through the same market circumstances over and over until we have a sequence of moves perfected). I prefer managing risk in our portfolios in the same way that I climb: with preparation, caution, and a strong dose of humility. That means we manage using the best tools that we have at our disposal and a strong team. We acknowledge that it is inevitable to slip and fall at times, but our tools (aka our risk management strategies, portfolio construction and asset allocation) are there to catch us and prevent a disastrous outcome. We know that sometimes despite our best planning that when (not if) we fall, we may not come through entirely unscathed.

Our Protection Strategies Cushion Downside Impact

We utilize a variety of tools to help cushion the downside impact on our portfolios when the markets slide or fall. Each one is designed with similar goals in mind, but utilized in differing degrees depending on the objectives of a portfolio. For example, in the Counsel Strategic Portfolios, we have an allocation to a trend following strategy - Counsel Global Trend Strategy. This strategy, which invests in a basket of globally-diversified exchange-traded funds, is designed to gradually switch between market segments towards safety as volatility and risk rises. The Global Trend Strategy’s peak to trough loss in 2020 was

-14.10%, compared to the benchmark MSCI World Index, which declined -26.27%. The strategy currently has 98% of its assets in U.S. treasuries – to preserve capital.

The Counsel Retirement Portfolios, meanwhile, have an allocation to a defensive equity strategy - Counsel Defensive Global Equity. This strategy invests in global equities, replicating the MSCI World index. It then uses a quantitative approach to systematically reduce exposure to equities during periods of sustained market downturns. This strategy is down -20.52% from peak trough this year versus the MSCI World Index at -26.27. It currently has 50% of its allocation in cash.

Within our discretionary IPC Private Wealth Program, we include an allocation to multi-strategy alternatives. Alternative assets tend to have a low correlation to equities and so help to smooth out returns. From peak to trough, the return for this strategy over the same period was -5.19%.

These are just three examples of a broad toolset that we use across our various portfolios. We strongly believe in diversification, not just at the asset class level, but across the types of strategies we use as we recognize that no one tool will work in every environment.

We will complete this climb and help our clients achieve their goals, but we all need to recognize that investing for the long term isn’t always fun. What is required most of all is patience, a long-term mindset and an ability to manage our fears. What I encourage investors to do is become comfortable with the uncomfortable. Markets will fluctuate as we will likely continue to see in the coming days and weeks.

The key is to work with your Advisor and create a detailed plan. Run scenarios around that plan and revisit it, at a minimum, annually or more frequently as life changes dictate. Lastly, measure your status against your plan, not some other irrelevant number such as a benchmark return.

Market and Economics: Oil Price Goes Negative

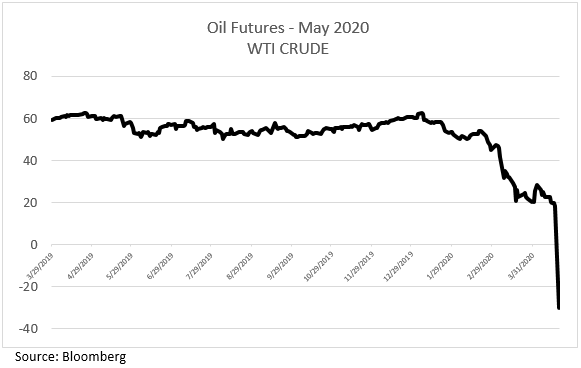

The word “unprecedented” is getting used quite a bit. There are some “unprecedented” aspects of this bear market, but the basic emotions of panic, fear, anticipation and greed are not. The past two weeks were no different. The week before Sunday, April 12, market participants bet on some sort of deal by oil-producing nations to reduce the supply of oil into global energy markets and balance supply and demand.

That anticipation led to oil prices (West Texas Intermediate – May Contract) rising from their March 30, 2020 lows of $20.09 per barrel to $28.34 a barrel (41% increase), only to fall to $18.27 at close on Friday, April 17. It was down much further on April 20 to -$30.40 (yes, you read that right - it’s a negative. That is not a mistake.).

A deal was reached two weekends ago. Saudi Arabia, Russia and the U.S. agreed to lead a multinational coalition to cut oil-production after demand dropped due to the coronavirus crisis and the Saudi-Russian feud devastated oil prices. As part of the agreement, 23 countries committed to collectively withhold 9.7 million barrels a day of oil from global markets. Unfortunately, the deal is insufficient to address the fact that supply currently exceeds demand by 30- 35 million barrels a day and, as a result, global oil prices fell to levels not ever seen. The build-up of crude oil is overwhelming storage space and clogging pipelines. The situation is so bad that traders of physical oil are bracing themselves for negative pricing, meaning that they will have to pay someone to take the oil. First negative interest rates, now someone will pay me to take barrels of oil off their hands. Interesting times. Free oil, anyone?

Global equity markets ended that last two weeks in a dramatic rebound, which leaves us with a confounding situation: soaring markets and a floundering economy. Some market participants are expecting a “V”-shaped recovery, supported by the liquidity injected by central banks (as the buyer of last resort) that is artificially propping up markets.

The prospect of social distancing measures being relaxed has traders looking forward to the global economic engine starting to rev up again. I am more cautious in my view. This isn’t a typical bear market where a liquidity crisis leads to a financial crisis. This is a medical crisis, so it cannot be solved by fiscal and monetary responses alone. The purpose of social distancing wasn’t to eliminate the prospect of a large percentage of the population becoming infected, rather, it was to increase the time that it took for large numbers of people to become infected so that we would not overwhelm our medical systems. To be truly free of COVID- 19, we need an effective vaccine and the time to inoculate everyone. If social distancing measures are relaxed too early, an increase in infection rates is inevitable. Coupled with the onslaught of negative economic data that is still to come, it will rock markets and we may re-test the March 23 lows.

Though it may sound negative, this type of market volatility is normal. When you look at previous crises, 1929, 1987 and 2008, there were bounces along the way to a new bull market being established, so be comfortable with the uncomfortable. Perhaps, I’m incorrect and “this time is different” (although I’ve heard that phrase many times before). I’m ok with that. I believe that we have the right balance between protecting investors in the event of further market falls while participating in the upside and generating positive returns as markets recover.

Final Thoughts

Investing for the long term shouldn’t be fun. Throughout my career, I’ve seen people confuse investing with trading and outright speculation. To me, speculation is gambling. If you don’t understand the risk, then you don’t understand the game that you are playing. Investing and speculation are two different activities and, frankly, neither should be “fun”.

Warren Buffett once said: "Investing is not trading and has a vastly different goal. Trading, when done well, is about taking measured risks for discrete periods of time at sufficient volume so as to generate profits, and typically involves wild swings in profitability. Investing is about minimizing risk to generate wealth over the long term, not generating short-term profits."

Thinking about risk isn’t fun. Ignoring risk or trying to defy it can be fun, that is if you are okay with the consequences.

So, as an investor, are you an Alex Honnold, or a Tommy Caldwell and Kevin Jorgeson? Are you okay with the thrills and challenges, rewards and the binary consequences of climbing without protection, like Alex? Or, are you like Tommy and Kevin, with the patience and determination to climb with protection, accepting that you will fall from time to time but, ultimately, over several years or even decades, you will reach your goals? The former may be more thrilling, but I prefer to live to climb another day. I hope you do, too.

Until next week, stay safe and be well.

Corrado Tiralongo

Chief Investment Officer

Counsel Portfolio Services | IPC Private Wealth

Click Here to Read Our Forward-Looking Statements Disclaimer