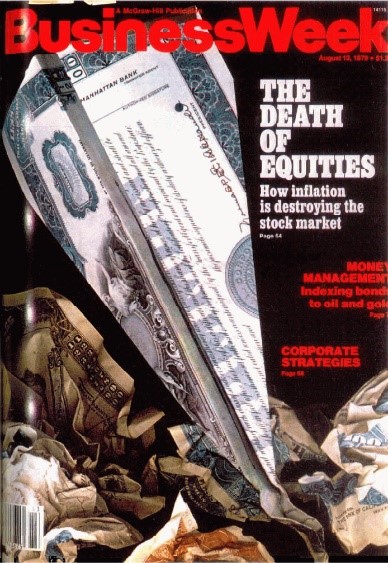

1963 to 1981. During this 18-year period, Canada and other developed nations suffered through the worst increase in inflation in their history. Interest rates rose more than ever before in Canada (surging from 1.3% to 12.12%) and inflation peaked at 12.65%. All of this happened during a slow economic growth environment. The combination of high inflation and low growth tends to be a terrible backdrop for equities. Imagine the investors who had bought equities for the long run, lived through all the ups and downs of the 1960s and 1970s, and had nothing to show for it in the end. Certainly, such an experience would dampen future expectations. Such widespread pessimism was captured on the cover of Business Week in 1979 as it famously proclaimed, “The Death of Equities”. Of course, these low expectations sowed the seeds for the bull market during the 1980s and 1990s.

Proclamations and Pundits

Nassim Taleb would have to be on anyone’s list of the top market forecasters over the past 25 years. In his book, The Black Swan: The Impact of the Highly Improbable, Mr. Taleb warned against the inability to foresee unusual events that have severe consequences. The book was published in 2007, just as the global financial crisis was beginning to gain momentum and worldwide financial systems were starting to crumble under the weight of a collapsing real estate market. After its release, Mr. Taleb was hailed as a visionary for seeing that the financial system was dangerously inter-connected and that giant institutions posed grave dangers. Ironically, Mr. Taleb warned repeatedly against relying on market and economic soothsayers whose proclamations usually emanated from severe cases of collective thinking and confirmation bias.

As we can see, history is littered with examples of reputable pundits and media outlets proclaiming a future outcome with certainty. Often those proclamations build upon each other, until the investor has no choice but to believe that the prediction is true. I think we can all appreciate that it is difficult to swim against the tide, especially when you are swimming alone.

When Narratives Go Viral

In his book, Narrative Economics, Robert Shiller writes that the human brain has always been highly tuned towards narratives, whether factual or not. Narratives “go viral” and spread far, even worldwide, with economic impact. The 1920-21 Depression, the Great Depression of the 1930s, the so-called “Great Recession” of 2007-09, are considered popular narratives of their respective times. The impact of non-factual narratives might be somewhat greater in today’s world than in decades past, since the advent of modern technology and social media. But we can also observe that narratives with no factual basis were widely disseminated and believed in past decades.

Let’s go a little deeper and look at human instinct. In his book, Factfulness, Hans Rosling’s discusses eleven instincts that trip up our perception of things. He proves that our guesses about how frequently something might occur or how risky things might be are often wrong. He also provides ten rules of thumb to guide us in making better decisions. His book is a reminder to investors to seek proof that the narrative or story is true, before acting on it.

Despite us understanding these facts about ourselves and having the tools to ensure that we do not fall prey to narratives, the financial markets are littered with forecasters – most with either an outwardly bullish (optimistic) or bearish (pessimistic) bias – and investors who blindly follow their narratives. Most forecasters missed the financial crisis when it hit because they were being too bullish, and some have been too bearish since, worrying that another systemic collapse is around the corner.

Here is a look at some of the most popular predictions as compiled by our sub-advisors:

- In 2010, billionaire entrepreneur, Richard Branson, issued a warning that “the next five years will see us face another crunch – the oil crunch,” predicting a severe supply shortage. Five years later, the price of oil was actually lower than it was then.

- In December 2007, Goldman Sachs chief investment strategist, Abby Joseph Cohen, suggested the S&P 500 would hit 1,675 by the end of 2008, a climb of 14% — it actually ended below 900.

- In September 2007, former Federal Reserve Chairman, Alan Greenspan, released a memoir called, The Age of Turbulence: Adventures in a New World. In the book, he claimed that the economy was heading towards two-digit interest rates due to expected inflationary pressures. According to Greenspan, the Fed would be compelled to drastically raise its target interest rate to fulfill the two percent inflation mandate. One year later, the Fed Funds rate was at historical lows, reaching the zero-lower bound shortly after.

-

James Glassman and Kevin Hassett's 1999 book, Dow 36,000, predicted that the Dow Jones stock index would more than triple in the years ahead. Even now, 21 years later, the index is only just three quarters to 36,000.

- Professor Ravi Batra wrote a book called, The Great Depression of 1990, predicting global turmoil. It was a New York Times number one bestseller in 1987, and Milton Friedman said he wouldn't "touch (the book) with a ten-foot pole".

- The stock market crash of 1929 and the subsequent Great Depression cost economist, Irving Fisher, much of his personal wealth and academic reputation. He famously predicted, nine days before the crash, that stock prices had "reached what looks like a permanently high plateau." Fisher stated on October 21 that the market was "only shaking out of the lunatic fringe" and went on to explain why he felt the prices still had not caught up with their real value and should go much higher. On October 23, he announced in a banker's meeting "security values in most instances were not inflated." For months after the crash, he continued to assure investors that a recovery was just around the corner.

What these predications and their narratives tell us, is that media outlets like to fan whatever flames are popular at the time. David Ragan, the lead portfolio manager for Counsel International Growth shares a great example of this. David points out that Brazil, Russia, India and China (commonly known as B.R.I.C. countries) were doing well from 1995 to 2013, coming off from a low valuation.

In 2001, when economist Jim O'Neill coined the acronym B.R.I.C. for the four countries that were deemed to be at a similar stage of newly advanced economic development, the media picked up on the B.R.I.C. acronym. This helped push those expectations and valuations past what should have been reasonable. David writes “I was in Brazil during this bubble and with the high valuation and general inflation, Sao Paulo started feeling like I was in Manhattan”.

Given that many of these bubbles, particularly in emerging markets, are commodities driven, they always (eventually) get pulled back to reality. With commodities, new capacity eventually comes online, increasing supply or the high prices of those commodities causes demand to fall.

A New Normal?

Investors usually start talking about “the new normal or “this time is different” after a period of strong performance or at the heels of poor results relative to the broad markets. They fall prey to non-factual narratives, pundit proclamations and even their own bias.

My team and I avoid these cognitive biases by understanding how the economic engine generally functions and the key drivers to asset class returns. By employing a systematic approach, as described in my previous commentary, The Blind Men and the Elephant, and employing our own versions of Hans Rosling’s Factfulness Rules of Thumbs, we ensure that we avoid the costly mistakes that less disciplined investors are destined to make.

The same thought process is involved when we hire investment managers to manage individual investment strategies. Return is the outcome of people and process, so we spend a great deal of time understanding the qualitative and quantitative drivers of performance that is encapsulated in our 8Ps investment process.

The result - whether you choose an individual investment strategy or one of our portfolios, you are getting a high-quality investment process, one that will serve an investor well over the long term. Now, all the investor has to do is hold onto those assets over the long term, which raises the likelihood of a successful investment experience via diversification, rebalancing and long-term compounding.

Corrado Tiralongo

Chief Investment Officer

Counsel Portfolio Services | IPC Private Wealth

Click Here to Read Our Forward-Looking Statements Disclaimer