counsel strategic canadians stay local or diversify - IPC Counsel Portfolio Services

| Counsel Portfolio Services added three new Canadian-focused investment solutions to its line-up: Counsel Canadian Conservative Portfolio, Counsel Canadian Balanced Portfolio, and Counsel Canadian Growth Portfolio. Each new portfolio adopts a strategic asset allocation strategy and has at least 70% of its assets allocated to Canadian securities. In addition to the domestically-biased, income-oriented Counsel Regular Pay Portfolio and Counsel Income Managed Portfolio (a tactical strategy), these solutions are designed to give you more choice and the ability to better target your financial goals. |

It comes as no surprise that many investors – regardless of where they live – tend to tilt their portfolios towards their home countries. It’s a sentiment referred to as the ‘home-bias’. Canadians are no different.

There are several reasons why people may choose a Canadian-centric portfolio: currency risk, preferential dividend tax treatment and familiarity-bias rank among the top. A bias to strong historical performance may also be a contributing factor.

![]() CURRENCY: Currency fluctuations can have a meaningful impact on the short-term performance of a portfolio. As such, an investor who is predominantly invested in Canada is able to take much of this risk off the table. “Currencies can be a problem,” says Kevin Hurlburt, Executive Vice President, Products and Services at Counsel Portfolio Services. “Currencies themselves can be influenced by significant factors, and don’t always correct back to fundamentals within a time-frame that is acceptable to many investors,” he explains.

CURRENCY: Currency fluctuations can have a meaningful impact on the short-term performance of a portfolio. As such, an investor who is predominantly invested in Canada is able to take much of this risk off the table. “Currencies can be a problem,” says Kevin Hurlburt, Executive Vice President, Products and Services at Counsel Portfolio Services. “Currencies themselves can be influenced by significant factors, and don’t always correct back to fundamentals within a time-frame that is acceptable to many investors,” he explains.

“As an industry, we talk about long-term investing, but the words ‘long-term’ mean different things to different people. Given a shorter time horizon, it’s a challenge because currencies can move significantly out of line relative to where they should be, and they can stay that way for quite some time.”

To minimize this risk over the shorter-term, you want to ensure that you have a hedging strategy in place. “Over the long-term, currencies do tend to equalize,” he adds. “Foreign currency risk will reduce as a major factor the longer you are able to hang onto your portfolio, but not everyone has 15 years or more as their time horizon.”

|

"Currencies themselves can be influenced by significant factors, and don’t always correct back to fundamentals within a timeframe that is acceptable to many investors.” |

![]()

PREFERENTIAL TAX CREDITS: Canadian dividends enjoy the best tax treatment of all income streams. So, if you’re income-oriented and invested in a non-registered portfolio, the dividend tax credit for eligible Canadian dividends is a strong incentive to keep your portfolio weighted towards Canadian dividend payers. It provides income stability and reduces the impact of fluctuations on your portfolio’s performance caused by other factors. Foreign dividend income is not eligible for this tax credit and may be subject to withholding tax.

![]() FAMILIAR INVESTMENTS: Your preference for staying home may be rooted in a behavioral bias. Was Canada the first place you invested and was it a good experience? You may, consciously or not, be anchored to that reference point – and using this first experience to guide your choices. Perhaps, you simply prefer to invest in companies that you know and deal with on a day-to-day basis?

FAMILIAR INVESTMENTS: Your preference for staying home may be rooted in a behavioral bias. Was Canada the first place you invested and was it a good experience? You may, consciously or not, be anchored to that reference point – and using this first experience to guide your choices. Perhaps, you simply prefer to invest in companies that you know and deal with on a day-to-day basis?

The constant exposure to companies you are familiar with, and knowledge of Canada’s comparatively strong corporate governance structures can have an influence on how you invest. This inclination to invest in that which you’re most familiar with is called familiarity bias, and it gives investors a degree of comfort.

![]()

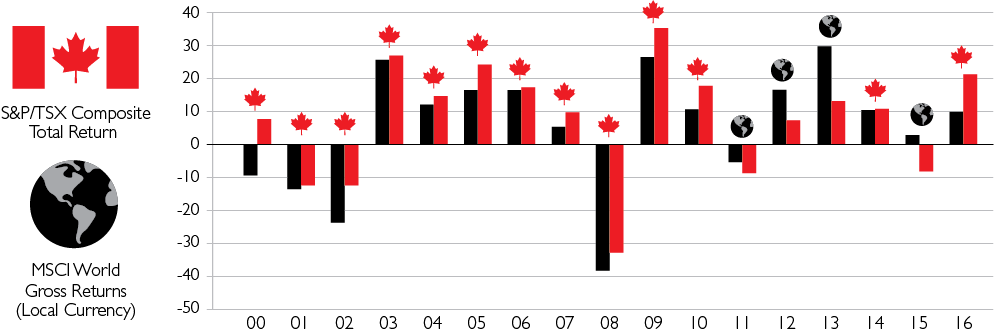

PAST PERFORMANCE: This is another influencing factor. “Canada is certainly a great place to invest. In the case of the stock market, in particular, Canada has shown remarkable resilience, outperforming in 13 of the 17 calendar years since the beginning of this century,” notes Kevin (see chart 1).

CHART 1: CANADA VS. THE WORLD - SINCE 2000

|

“Canada has shown remarkable resilience, outperforming in 13 of the 17 calendar years since the beginning of this century.” |

KNOW THE RISKS

Relying on historical performance should not be a core reason for investors to stay home. There are caveats to be considered.

There are several reasons why Canada has fared well in the past, Kevin explains. Relative to other markets, Canada was less impacted by the 2000-2002 tech-wreck because of its comparatively lower exposure to technology companies. In the recovery years that followed, higher oil prices drove Canada’s performance. Canada also emerged from the 2008 financial crisis fairly unscathed due, in part, to the strength of our financial system. “These were some important factors, forces which may not necessarily be repeated,”

he adds citing why Canadians would consider diversifying.

Studies show that diversification reduces risk by spreading it across geographies and asset classes so no one single event is able to derail your investment plans.

It’s important to recognize that the Canadian equity market is small relative to major world markets. In terms of market capitalization, Canada accounts for less than 4% of the world’s total market cap, while our neighbour to the south weighs in at just under 60%1. Because of this, plus the fact that close to 75% of our market is concentrated to just a few economic sectors – financials, energy, and materials – Canadians who stay home may be missing out on opportunities to invest in great companies elsewhere and may sacrifice some returns in the long-run.

Similarly, when looking at fixed-income opportunities, he says “investors could enjoy better corporate bond yields if they were to include the North American market as a whole.”

Beyond that, Kevin adds, “if you look at where growth is coming from today, Canada is not the strongest performing economic or equity market in the world. So, if you’re excluding global markets from your portfolio, you want to make sure you’re still finding ways to participate in the growth.”

The Counsel Canadian Strategic Portfolios have an exposure of up to 30% to foreign equities, including exposure to higher yielding U.S. dollar fixed income securities to provide investors with some downside protection. To minimize currency risk, we’ve added a dynamic currency hedge strategy on the portfolios’ U.S. dollar exposure.

CHOOSE A STRATEGY THAT FITS YOUR PREFERENCE, GOALS, AND OBJECTIVES

Choosing the right investment strategy or portfolio allocation boils down to several factors, including your investment goals, personal preferences, and level of tolerance for risk. “The informed investor should understand that, over the long term, investing with a more global perspective gives you opportunities for greater diversification and greater enhancement of returns through access to a much broader selection of investments and markets.”

Still, if a Canada-centric portfolio is right for you, there are ways to help you achieve your personal goals while respecting this personal preference. Working with an Advisor to determine exactly what is right for you as an investor is a key part of picking an appropriate portfolio.

|

ABOUT COUNSEL’S INVESTMENT SOLUTIONS As a comprehensive portfolio service, Counsel Portfolio Services offers investors a wide range of investment solutions (core strategies: strategic, tactical, retirement) to help target and reach their |

Ask your Advisor about the investment strategy

or portfolio structure that can best target your

investment goals and objectives.

To view as a PDF, click here.

1. Source: MSCI World Index, Morningstar Direct.

DISCLOSURE

This report may contain forward-looking statements which reflect current expectations or forecasts of future events. Forward-looking statements include statements that are predictive in nature, depend upon or refer to future events or conditions, or include words such as: “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates”, “preliminary”, “typical” and other similar expressions. In addition, these statements may relate to future corporate actions, future financial performance of a fund or a security and their future investment strategies and prospects. Forward-looking statements are inherently subject to, among other things, risks, uncertainties, and assumptions which could cause actual events, results, performance or prospects to differ materiality from those expressed in, or implied by, these forward looking statements. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, the volatility of global equity and capital markets, business competition, technological change, changes in government regulations, changes in tax law, unexpected judicial or regulatory proceedings, catastrophic events and the ability of the investment specialist to attract or retain key employees.

The foregoing list of important risks, uncertainties and assumptions is not exhaustive. Please consider these and other factors carefully and not place undue reliance on forward-looking statements. The forward-looking information contained in this report is current only as of the date of this report. There should not be an expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise. Commissions, trailing commissions,managementfees and expenses all may be associated with mutual fund investments. Please read the Simplified Prospectus before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. The indices cited are widely accepted benchmarks for investment performance within their relevant regions, sectors or asset class, represent non-managed investment portfolios, exclude management fees and expenses related to investing in the indices, and are not necessarily indicative of future investment returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.