To view as a PDF, click here.

WHAT IS HAPPENING?

In response to U.S. defence official documents, which state that North Korea has the capability to miniaturise a nuclear weapon and place it on one of its missiles, U.S. President, Donald Trump, issued an ultimatum for North Korea to reduce its testing or “face fire and fury like the world has never seen.” North Korean leader, Kim Jong-un, retaliated by threatening a strike on Guam, a U.S. Pacific territory and a major American military base. Inflammatory news headlines aside, there are few signs that the U.S. is planning a first strike on North Korea or that Kim will make good on threats to hit Guam.

Still, the antagonistic exchange between the two leaders appeared like a market grey swan (a known risk that’s always lurked in the background) causing uncertainty. Market volatility, which was already on the rise in June, increased dramatically last week. The broad-based S&P500 Index fell 1.4% on August 10, the largest downward move of the year, while Canadian stocks had their biggest weekly decline since June.

VIX is the ticker symbol for the Chicago Board Options Exchange (CBOE) Volatility Index, which shows the market’s expectation of 30-day volatility. A higher number represents greater anxiety in the markets.

WHAT DOES IT MEAN TO YOUR PORTFOLIO?

There are three main news cycles that generate interest among investors: corporate, political, and geopolitical.

With the winding down of earnings season, and the U.S. Congress on vacation until September, it’s the geopolitical news that’s dominating headlines.

Economically, the greatest concern out of the current news cycle is for South Korea, which accounts for nearly 2% of the world’s economy and is home to companies such as Samsung Group and Hyundai Motor Company. A drop in business activity due to a war will have a terrible human cost and will affect growth in regional and global markets, negatively impacting equity markets. However, we do not expect war to breakout in the region. We recommend investors exercise patience and stay calm rather than get caught up in the headlines.

Much like we’ve seen with many other geo-political events, hopefully the volatility triggered by this news cycle will be short-lived. We expect to see a flight to safe haven assets such as fixed income, the U.S. dollar and the Swiss franc. We also expect price increases in commodities such as oil, as conflict concerns usually translate into higher demand for resources.

WHAT ARE WE DOING?

For now, we continue to stick to our disciplined investment strategy. Our portfolios are structured with a balance of fixed income and equity exposure to help minimize risk. It’s at times like these that we are grateful for the fixed income exposure, which can act as a shock absorber to a short-term downturn in equity markets.

The fundamentals of the global economy are good. Corporate earnings and revenues are strong. Monetary policy is still accommodative despite rate increases in North America. The breadth of the market is still strong at 68% advancers, but we are likely overdue for a short-term correction.

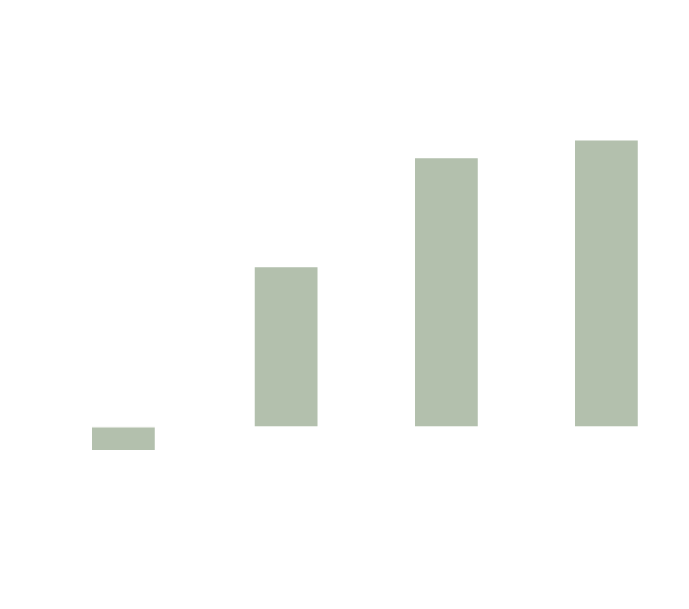

Historically, as the chart here suggests, markets have reacted strongly in the wake of American-led military operations, should one occur.

We will continue to see rumours and troubling headlines circulate over the next few weeks. This may cause even more volatility. The next headline could point to problems in Venezuela, Iran, Russia, Syria, or even in the U.S., as they start to focus on the debt ceiling. We consider this normal and we’ve been through it many times over the last few years.

Along with the investment specialists for your portfolio, we are keeping an eye on the news cycle, but we will stay above the noise and not be distracted by it.

|

Our goal is to mitigate the risks in your portfolio as we help you achieve your return expectation. |

As part of our process, we are reviewing the portfolios for opportunities to rebalance (buy low, sell high) or to adjust our U.S. dollar hedge positions. We also have specific strategies in place for our portfolios that allow our investment specialists to preserve capital by switching out of volatile market sectors during periods of market stress. Our goal is to mitigate the risks in your portfolio as we help you achieve your return expectation.

By and large, we believe what we are seeing today is simply sabre rattling between the U.S. and North Korea, and will unlikely result in any meaningful deterioration in the global growth picture. This could well be just a tempest in a teapot and will soon pass.

DISCLOSURE

Trademarks owned by Investment Planning Counsel Inc. (IPC) and licensed to its subsidiary corporations. Investment Planning Counsel, is a fully integrated Wealth Management Company. Mutual Funds available through IPC Investment Corporation and IPC Securities Corporation. Securities available through IPC Securities Corporation, a member of the Canadian Investor Protection Fund. Insurance products available through IPC Estate Services Inc. Counsel Portfolio Services is a wholly-owned subsidiary of IPC.

This report may contain forward-looking statements which reflect current expectations or forecasts of future events. Forward-looking statements include statements that are predictive in nature, depend upon or refer to future events or conditions, or include words such as: “expects”, “anticipates”, “intends”, “plans”, “believes”, “estimates”, “preliminary”, “typical” and other similar expressions. In addition, these statements may relate to future corporate actions, future financial performance of a fund or a security and their future investment strategies and prospects. Forward-looking statements are inherently subject to, among other things, risks, uncertainties and assumptions which could cause actual events, results, performance or prospects to differ materiality from those expressed in, or implied by, these forward looking statements. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors in North America and internationally, interest and foreign exchange rates, the volatility of global equity and capital markets, business competition, technological change, changes in government regulations, changes in tax law, unexpected judicial or regulatory proceedings, catastrophic events and the ability of the investment specialist to attract or retain key employees. The foregoing list of important risks, uncertainties and assumptions is not exhaustive. Please consider these and other factors carefully and not place undue reliance on forward-looking statements. The forward-looking information contained in this report is current only as of the date of this report. There should not be an expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the Simplified Prospectus before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that would have reduced returns. The indices cited are widely accepted benchmarks for investment performance within their relevant regions, sectors or asset class, represent non-managed investment portfolios, exclude management fees and expenses related to investing in the indices, and are not necessarily indicative of future investment returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.